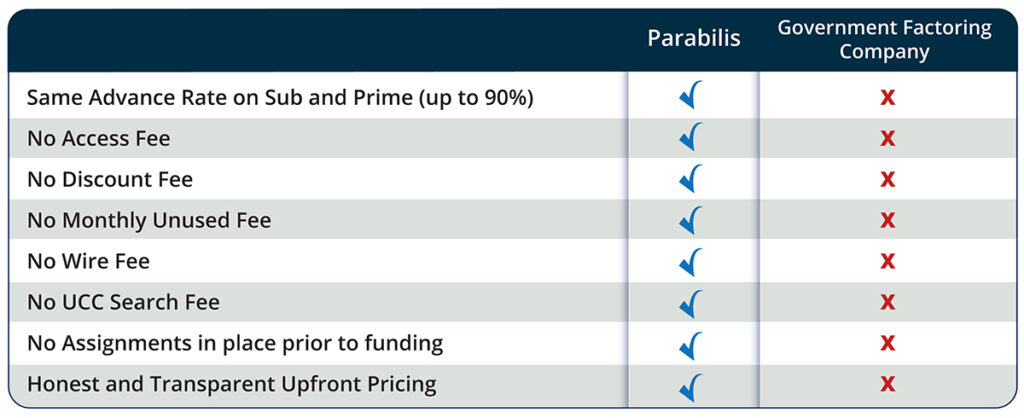

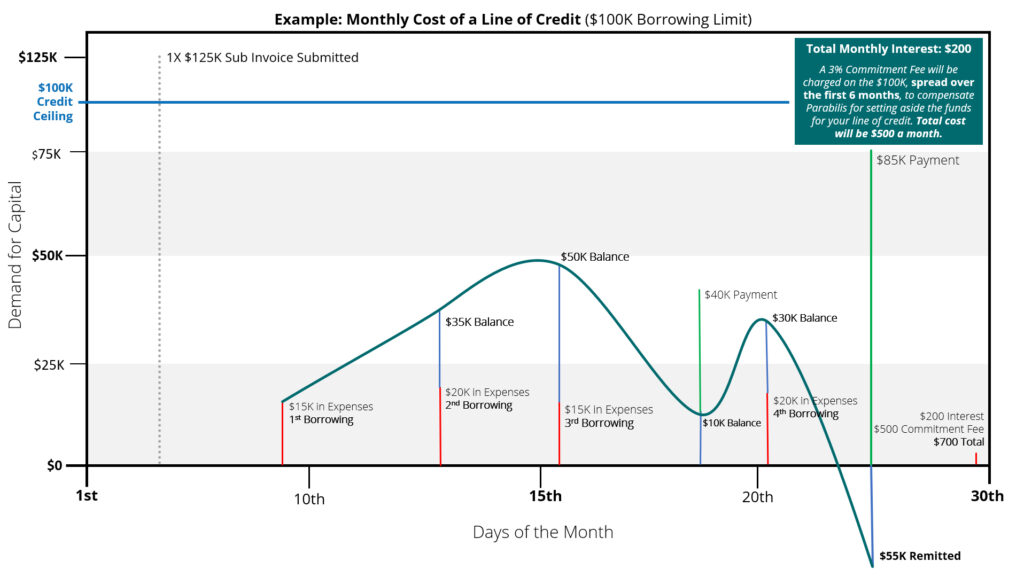

Revolving Lines of Credit – Just in Time Financing

Just in Time Inventory Management grew in popularity in the mid 1970’s; it’s a popular business management concept built on maintaining a supply of goods that perfectly meets the market demand “just in time” thereby reducing both labor and product waste and in turn, reducing expenses. We view our lines of credit as “just in time” business financing, reducing the interest expense of paying for capital the business doesn’t need. As outlined in parts 1 and 2 of this series, there are many inflexible financing options available to the government contracting market, the most common of which is factoring. We often refer to a line of credit (LOC) as a more flexible solution than factoring, but what does flexibility mean to businesses with a varying month-to-month cash flow requirement? The chart below represents a revolving line of credit balance with a 15% annual interest rate over the course of a typical month. In our example, this client is borrowing against a single $125K sub contractor invoice that pays in two separate amounts each month. When borrowing with a line of credit, draws are made to cover expenses which increase the balance, and periodic contract payments are received which decrease the balance (Exhibit A). This results in a pattern of rising and falling balances to meet the specific needs of the borrower. This reduces the overall cost of capital because, unlike with factoring where borrowers must sell entire invoices, borrowers only borrow what they need when they need it (i.e., Just in Time), significantly reducing their cost of capital.

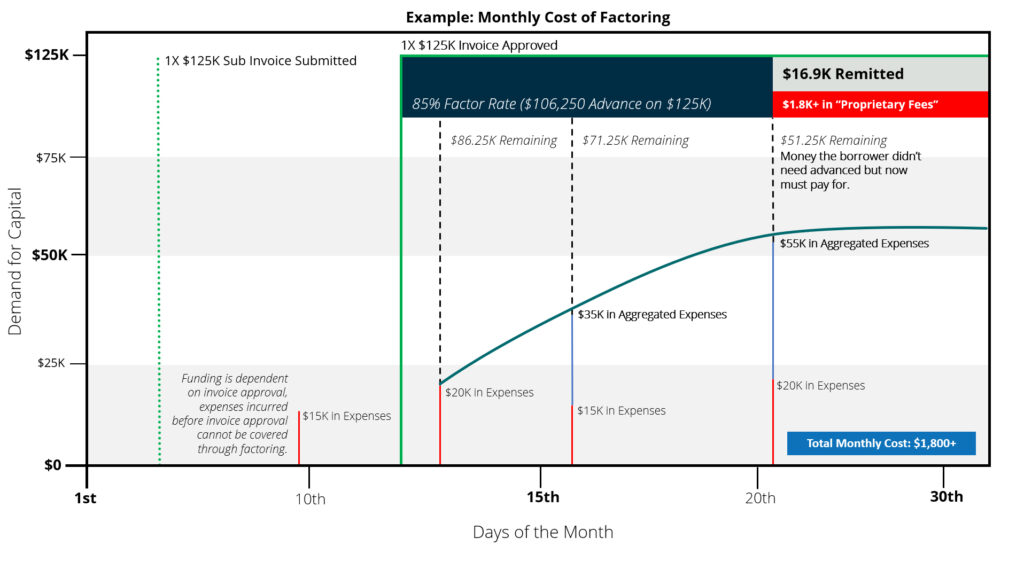

Factoring arrangements, as outlined in part 1, do not provide the borrower with the flexibility to borrow only what is needed (Exhibit B). Invoices are sold in their full amounts and the “proprietary” fees are deducted once the payments flow to the factoring company. This leads to an increased cost of capital for the borrower.

Confused by factoring? You should be. The factoring advance is dependent on the timing of the invoice’s approval, therefore any expenses incurred before the approval date will need to be covered by cash on hand. Once the invoices are approved, the factoring company will purchase the invoices and wire the funds, typically at a rate of 80%-85% of the total invoice amount. The catch here is that you will be factoring the entire invoice, regardless of what you actually need to cover monthly expenses. This is one of the reasons why factoring is significantly more expensive. In the above example the borrower only needed to cover monthly expenses of $70K, however, in order to do this, they needed to factor their entire $125,000 invoice. This resulted in factoring $55K more than they needed, which will cost them significantly more per month to continue factoring compared to borrowing exactly what they need with a revolving line of credit. Not to mention, they needed $15K before the invoice was approved, factoring is not able to help them cover this expense. Inflexible financing results in higher costs – a revolving line of credit with Parabilis is more flexible, more affordable, more transparent, and Just in Time. We work to develop a long-term partnership with our clients, function as a resource, and grow side by side, in addition to saving you money on interest.